Bitcoin correlation with stocks hits record highs

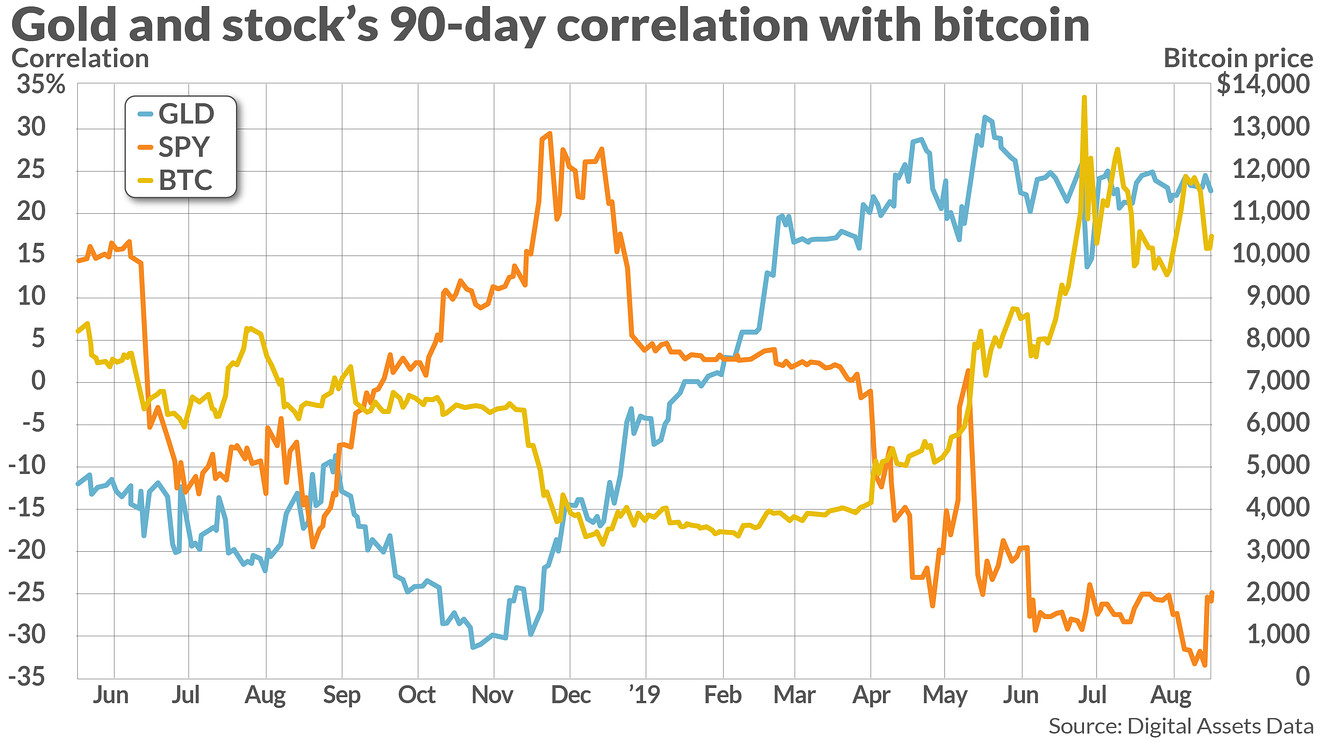

Bitcoin is no longer behaving as the uncorrelated diversifier it once promised. In early 2026, the 30-day correlation coefficient between Bitcoin and the S&P 500 surged to 0.74, marking the highest level recorded this year [src-serp-1]. This structural shift means that when equities sell off, crypto assets are now moving in lockstep, stripping investors of the traditional hedging benefits that defined the asset class in previous cycles.

The data from NewHedge confirms that Bitcoin and the S&P 500 have displayed one of the strongest correlations among major assets, with the 30-day rolling correlation consistently exceeding 70% [src-serp-2]. This tight coupling suggests that institutional adoption and ETF flows have fundamentally altered how Bitcoin reacts to macroeconomic news. The asset is now pricing in interest rate expectations and earnings guidance with the same sensitivity as a tech stock.

Even more alarming are reports indicating that Bitcoin’s correlation with stocks has hit a record 0.96 during specific volatility spikes [src-serp-3]. At this level, the distinction between "risk-on" crypto and traditional equities effectively vanishes. For portfolio managers, this means that allocating to crypto no longer reduces overall portfolio variance; it simply adds another layer of equity-like exposure.

The implications for 2026 portfolio construction are stark. If Bitcoin tracks the S&P 500 with a coefficient approaching unity, it cannot serve as a hedge against market downturns. Investors seeking diversification must look beyond simple crypto allocations or accept that their "alternative" assets are now fully integrated into the traditional financial system's risk profile.

Bitcoin ETFs and institutional equity overlap

The approval and subsequent growth of Spot Bitcoin ETFs have fundamentally altered the structural relationship between digital assets and traditional finance. By channeling institutional capital through regulated equity vehicles, the crypto market has shed its status as an isolated niche and integrated into the broader portfolio management framework. This integration is not merely symbolic; it has created a mechanical linkage that forces price discovery to align with broader market sentiment.

This structural shift is evident in the data. According to Bloomberg, the 30-day correlation coefficient between Bitcoin and the S&P 500 recently surged to 0.74, marking the highest level recorded this year. Such a high coefficient indicates that Bitcoin is no longer acting as a distinct, uncorrelated asset class but is instead moving in tandem with risk-on tech equities. The mechanism is straightforward: institutional investors treating Bitcoin exposure through ETFs often rebalance these positions in response to macroeconomic signals that simultaneously drive traditional equity markets.

The implications for portfolio construction are significant. When crypto correlates with the S&P 500, its utility as a diversifier diminishes during market stress. Investors seeking true uncorrelated returns may find that traditional hedges are less effective than previously assumed. This convergence suggests that the "new risk profile" for crypto is now inextricably linked to the health and volatility of the broader equity market, rather than standing apart from it.

Mining stocks vs. spot bitcoin price action

The correlation between spot Bitcoin and mining equities is not a fixed constant; it is a leverage mechanism that amplifies both gains and losses. While spot ETFs track the underlying asset with minimal friction, mining stocks operate as leveraged bets on the hash rate, energy costs, and corporate balance sheets. This structural difference creates a divergence in price action that becomes starkly visible during market stress.

Historical data underscores this asymmetry. According to Fidelity, a bitcoin mining stock that outperformed Bitcoin in 2025 subsequently dropped over 89% when Bitcoin began its decline in October 2025 [[src-serp-5]]. This decoupling occurs because mining companies face fixed operational costs (electricity, hardware maintenance) while their revenue is tied to a volatile asset. When Bitcoin’s price falls below the cost of production for marginal miners, the equity value can collapse far faster than the asset price itself.

To understand the risk profile, we must compare the structural characteristics of these three distinct asset classes. The table below contrasts Spot ETFs, Mining Stocks, and Blockchain Technology firms across correlation, volatility, and income generation.

The data reveals that mining stocks offer higher beta exposure to Bitcoin but introduce significant idiosyncratic risk. With Bitcoin’s annualized volatility dropping to 38% in early 2026—the lowest level in over a decade—the margin for error in leveraged equities shrinks further [[src-serp-8]]. Investors seeking pure price exposure should look to spot ETFs, while those willing to accept operational risk for potential alpha must monitor the spread between Bitcoin’s price and the breakeven cost of production for major miners.

Portfolio implications for 2026 investors

The structural shift in 2026 demands a fundamental rethinking of position sizing. As Bitcoin’s correlation with the S&P 500 tightens, the traditional narrative of crypto as a non-correlated hedge dissolves. Investors can no longer rely on digital assets to provide diversification benefits during equity drawdowns. Instead, crypto equities and spot assets now move in tandem with broader market liquidity and risk sentiment.

To manage this heightened systemic risk, portfolio construction must prioritize precise allocation over speculative exposure. A standard 5-10% crypto allocation is no longer sufficient to offset equity volatility; it now acts as a leveraged bet on risk-on flows. Investors should treat crypto exposure as a satellite position within a broader tech-heavy portfolio, ensuring that a single macro shock does not disproportionately impact overall portfolio stability.

Live market data confirms this convergence. The following widgets track the current price action of Bitcoin and the S&P 500 ETF (SPY), illustrating the tight coupling of these assets in real-time.

The risk profile of 2026 favors disciplined rebalancing. When correlations spike, the only reliable defense is strict position sizing and reduced leverage. Relying on past cycles where crypto moved independently is a dangerous strategy for current market conditions.

Tracking the correlation in real-time

Understanding the dynamic relationship between crypto and traditional equities requires monitoring technical indicators that capture momentum divergence. The chart below visualizes the price action of Bitcoin, allowing investors to spot moments of decoupling or sudden alignment with broader market trends.

Frequently asked questions on crypto equity ties

What is the current correlation between Bitcoin and the S&P 500?

As of early 2026, the 30-day rolling correlation between Bitcoin and the S&P 500 has surged to approximately 0.74, with spikes reaching 0.96 during periods of high volatility. This represents a structural break from historical norms where Bitcoin often acted as an uncorrelated asset. The correlation is driven by institutional ETF flows that tie Bitcoin's price discovery to broader macroeconomic signals and equity market sentiment.

Why has Bitcoin's correlation with stocks increased?

The primary driver is the integration of Spot Bitcoin ETFs into traditional portfolio management frameworks. Institutional investors rebalance these positions in response to the same macroeconomic data (interest rates, inflation, earnings) that drives equity markets. This mechanical linkage forces Bitcoin to price in risk-on/risk-off dynamics similarly to tech stocks, reducing its utility as a diversifier.

How does this correlation impact portfolio diversification?

High correlation diminishes Bitcoin's effectiveness as a hedge against equity drawdowns. In a market downturn, Bitcoin is likely to decline alongside the S&P 500 rather than providing offsetting returns. Investors seeking true diversification may need to look beyond crypto allocations or accept that their "alternative" assets are now part of the broader equity risk profile.

What is the outlook for Bitcoin's correlation in 2026?

Analysts project that correlation will remain elevated as institutional adoption deepens. While short-term volatility may cause temporary decoupling, the long-term trend suggests Bitcoin will continue to track broader market liquidity and risk sentiment. Investors should monitor correlation coefficients closely, as spikes above 0.80 indicate a high risk of simultaneous asset class declines.

No comments yet. Be the first to share your thoughts!