Understand the new 2026 reporting rules

The 2026 crypto tax laws mark a significant shift in how cryptocurrency transactions are reported to the IRS. For years, many investors relied on the fact that brokers did not report their cost basis, making it difficult for the agency to verify gains. Under the new rules, this changes starting January 1, 2026.

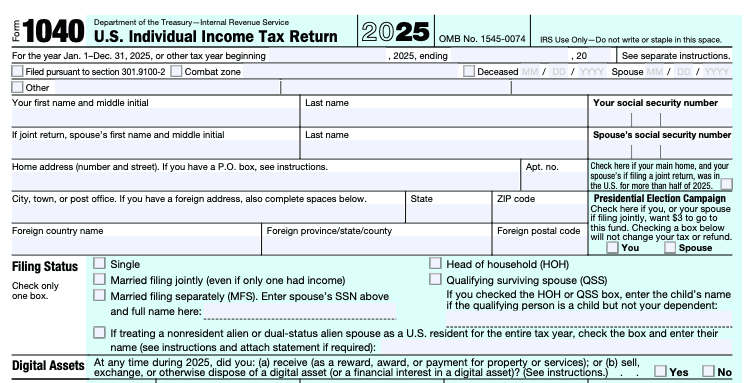

The central document for the 2026 filing season is Form 1099-DA. This form consolidates your digital asset transaction history, including gross proceeds and the newly required cost basis. Instead of piecing together data from multiple exchanges or relying solely on internal records, you will receive this standardized form from your broker.

This shift means you can no longer ignore the cost basis of your assets. If your broker reports the basis, the IRS will have a record of your entry price. This reduces the margin for error and ensures that gains or losses are calculated accurately based on actual purchase prices rather than estimates.

To comply with the 2026 crypto tax laws, start by reviewing your 1099-DA forms as soon as they are issued. Compare the reported cost basis against your own records to ensure accuracy. Any discrepancies should be resolved before filing to avoid potential audits or penalties.

Gather your transaction records

Filing under the 2026 crypto tax laws requires a complete dataset before you can calculate your liability. The IRS has tightened reporting requirements, making it essential to collect accurate records from every source where you held or traded digital assets.

Start by logging into each centralized exchange you used. Under the new rules, platforms are required to issue Form 1099-DA to report your proceeds. Download these forms and any supplementary transaction history reports they provide. This data serves as the primary audit trail for your trades and sales.

Next, export your data from personal wallets and decentralized exchanges. Unlike centralized platforms, wallets do not automatically issue tax forms. Use your wallet’s export feature or a compatible tool to generate a CSV of all incoming and outgoing transactions. Ensure you capture the date, amount, and fair market value in USD at the time of each transaction.

Finally, organize these records by asset type and wallet address. The IRS now requires cost basis tracking to be separated for each wallet or exchange. Keeping your data segmented from the start will prevent errors when you later reconcile your totals against the official 1099-DA forms.

Log into every exchange you used in 2025. Navigate to the tax or reports section and download your Form 1099-DA and full transaction history CSV files.

For non-custodial wallets and DeFi platforms, use the wallet’s built-in export tool or a blockchain explorer to create a complete transaction log. Include all incoming and outgoing transfers.

Create separate folders or spreadsheets for each exchange and wallet. The IRS requires cost basis to be tracked separately per location, so keep these datasets distinct.

Calculate gains and losses per wallet

Under the 2026 crypto tax laws, the IRS requires you to track the cost basis of your digital assets separately for each wallet or exchange. This is not a suggestion; it is a strict compliance rule that fundamentally changes how you calculate your gains and losses.

Previously, many taxpayers netted gains and losses across all their holdings to find a single bottom line. That approach is no longer valid. You must now treat each wallet as a distinct ledger. If you moved Bitcoin from Wallet A to Wallet B, the transaction itself is not a taxable event, but the cost basis must remain attached to that specific chain of custody.

This separation prevents you from offsetting a loss in one wallet against a gain in another unless the assets are identical and held in the same account. For example, if you sold Ethereum at a loss in an exchange account and bought it back in a self-custody wallet, you generally cannot use that loss to offset gains in the new wallet. The IRS views these as separate tax lots.

To stay compliant with these 2026 crypto tax laws, you need a system that tracks cost basis per wallet. Use the checklist below to ensure your calculations are accurate before filing.

-

Identify every wallet and exchange used during the tax year.

-

Record the original purchase price and date for every asset in each wallet.

-

Calculate the gain or loss for each specific asset within its own wallet.

-

Do not net losses across different wallets unless the assets are identical and in the same account.

File Form 1099-DA with your return

Starting in the 2026 tax year, the Internal Revenue Service requires centralized cryptocurrency exchanges to issue Form 1099-DA for digital asset transactions. This form replaces the previous patchwork of reporting mechanisms and serves as the primary document for calculating your tax liability on crypto sales, trades, and transfers.

To comply with the 2026 crypto tax laws, you must integrate the data from this form into your tax software. Most major platforms will generate the 1099-DA automatically, but you are responsible for verifying that the reported proceeds and cost basis match your actual transaction history. Errors on the form can trigger audits, so cross-reference the figures against your own records before filing.

When you file, enter the information from Form 1099-DA directly into the designated section of your tax return. Ensure that any off-exchange transactions or DeFi activities not covered by the broker’s form are reported separately to avoid underreporting. The IRS uses this data to reconcile your return, so accuracy is essential to avoid penalties.

Avoid these common 2026 crypto tax filing mistakes

Navigating 2026 crypto tax laws requires precision. Even minor oversights can trigger audits or unnecessary penalties. Below are the most frequent errors taxpayers make when reporting digital assets, along with how to correct them.

Ignoring DeFi and Staking Rewards

Many filers overlook income generated from decentralized finance (DeFi) protocols, liquidity pools, and staking. The IRS treats crypto as property; therefore, any reward received through staking or yield farming is taxable income at the fair market value when received.

To avoid this mistake, use a crypto tax tool that integrates with your DeFi wallets. These tools can scrape on-chain data to identify unstaked rewards, providing a complete record of your taxable events. Failing to report this income is a common trigger for IRS notices.

Misapplying the Wash-Sale Rule

A widespread misconception is that the wash-sale rule applies to cryptocurrency. It currently does not. Under existing IRS guidance, you can sell a crypto asset at a loss and immediately repurchase it to claim that loss on your taxes.

While this provides a strategic advantage for tax-loss harvesting, it is important to stay informed. Future legislation could change this treatment. For now, ensure your tax software correctly identifies crypto sales as exempt from wash-sale restrictions to maximize your deductions.

Failing to Track Cost Basis per Wallet

Starting in 2025 and continuing into 2026, the IRS requires taxpayers to track the cost basis of digital assets separately for each wallet or exchange. Mixing assets from different sources can lead to incorrect gain/loss calculations.

Keep meticulous records of your acquisition dates and prices for every asset in every wallet. When filing, ensure your tax preparer or software segregates these calculations. Consolidating data from multiple exchanges without proper cost-basis tagging can result in overreporting or underreporting your taxable income.

No comments yet. Be the first to share your thoughts!